Decentralized Finance, or DeFi, has fundamentally transformed how people access financial services. At its core, DeFi lending platforms allow users to earn interest on their cryptocurrency holdings or borrow assets without relying on traditional banks. Instead of dealing with paperwork, credit checks, and intermediary delays, smart contracts automate the entire process—matching borrowers with lenders directly through blockchain technology. If you’ve ever wondered how you could earn passive income on your crypto holdings or access liquidity without selling your assets, DeFi lending offers a compelling alternative to conventional finance.

This guide breaks down everything you need to know about DeFi lending platforms, from the basic mechanics to practical steps for getting started. Whether you’re a cryptocurrency holder looking to maximize your returns or simply curious about decentralized finance, this article will give you a solid foundation for understanding this rapidly evolving space.

What Is DeFi Lending and How Does It Work?

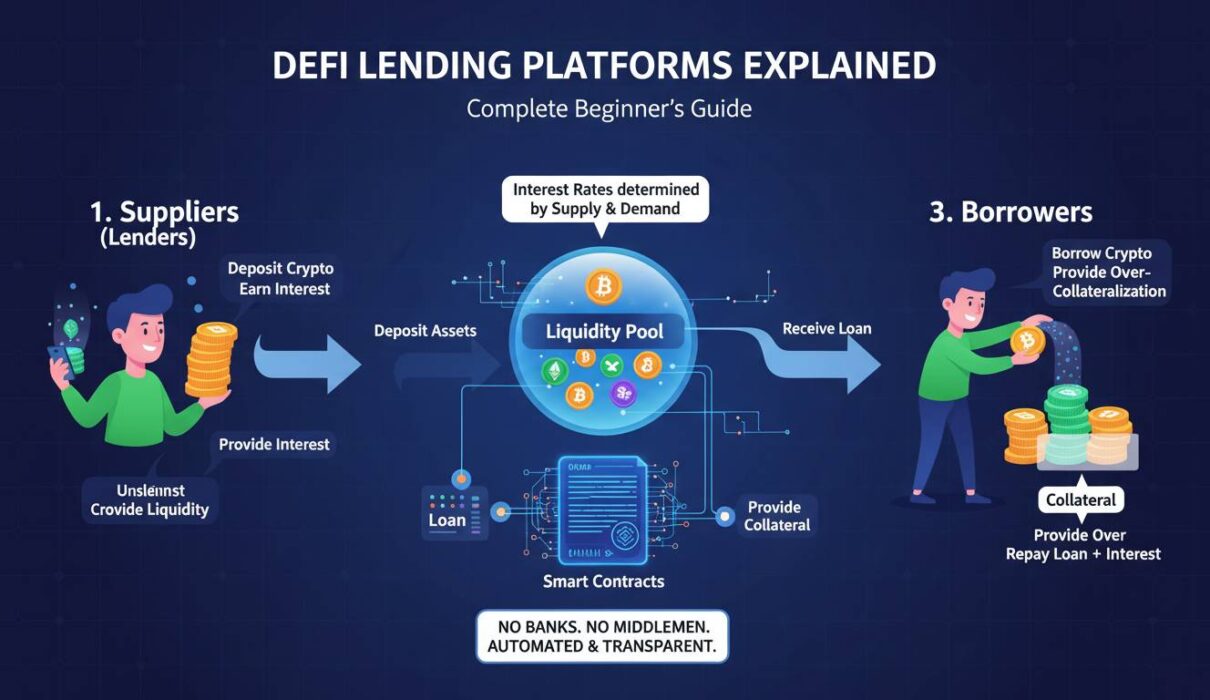

DeFi lending refers to the practice of lending and borrowing cryptocurrency through decentralized protocols—software applications built on blockchain networks that operate without central authorities. These platforms use smart contracts, which are self-executing programs that automatically enforce the terms of a loan when predetermined conditions are met.

The process works like this: when you deposit cryptocurrency into a DeFi lending protocol, your funds go into a liquidity pool. Borrowers can then draw from these pools by providing collateral that exceeds the value of their loan. Interest rates are determined algorithmically based on supply and demand—when more people want to borrow an asset, interest rates rise; when supply exceeds demand, rates fall.

Unlike traditional banks, DeFi platforms don’t conduct credit checks or require identity verification in most cases. Instead, they rely entirely on collateral. If a borrower’s collateral value drops below a certain threshold due to market volatility, the protocol automatically liquidates their collateral to protect lenders. This system, known as over-collateralization, ensures that lenders are protected even without knowing who they’re lending to.

The entire process happens on public blockchains, meaning anyone can verify transactions and audit the code. Major networks like Ethereum, Solana, and Polygon host most DeFi lending activity, with Ethereum holding the largest share of total value locked in lending protocols.

Key Concepts You Need to Understand

Before using DeFi lending platforms, several fundamental concepts merit understanding to navigate this space effectively.

Collateral serves as the security for loans. To borrow assets on DeFi platforms, you must deposit cryptocurrency worth more than what you’re borrowing—typically 110% to 150% of the loan value. This over-collateralization protects lenders from losses if borrowers default. Popular collateral assets include Ethereum (ETH), Wrapped Bitcoin (WBTC), stablecoins like USDC, and other liquid tokens.

Annual Percentage Yield (APY) represents the return you earn on your deposited funds. Unlike simple interest, APY accounts for compound interest, showing your actual yearly return including interest on your interest. DeFi lending APYs fluctuate constantly based on market conditions, sometimes ranging from 1% to 15% or higher for volatile assets.

Liquidity Pools are the reservoirs of cryptocurrency that power DeFi lending. When you deposit funds, you’re adding to a pool that borrowers draw from. In return for providing liquidity, you earn a share of the interest paid by borrowers. These pools ensure that borrowing remains possible at any time, provided sufficient liquidity exists.

Loan-to-Value (LTV) Ratio determines how much you can borrow against your collateral. If you deposit $1,000 worth of Ethereum with a 75% LTV, you could borrow up to $750 worth of another asset. Different assets have different LTV thresholds based on their volatility—more stable assets typically allow higher borrowing limits.

Liquidation occurs when a borrower’s collateral falls below the required threshold due to price movements. The protocol automatically sells portions of the collateral to repay the loan and protect lenders. This mechanism maintains the system’s solvency but can result in borrowers losing their collateral if prices drop rapidly.

Major DeFi Lending Platforms

Several platforms have emerged as leaders in the DeFi lending space, each offering distinct features, supported assets, and risk profiles.

Aave stands as one of the largest and most established DeFi lending protocols. Originally launched as ETHLend in 2017 before rebranding to Aave in 2018, the platform pioneered the concept of flash loans—uncollateralized loans that must be repaid within a single blockchain transaction. Aave supports over 20 collateral types and has facilitated billions in total borrowed volume. The protocol is governed by AAVE token holders, who vote on important protocol changes and parameter adjustments.

Compound was one of the first major DeFi lending platforms, launching in 2018 and popularizing the algorithmic interest rate model used by many subsequent protocols. Compound’s simplicity and audited code made it a trusted choice for many users. The platform rewards suppliers and borrowers with COMP tokens, creating an additional incentive for participation. As of early 2025, Compound remains one of the most actively used lending protocols, though it has faced some governance challenges.

MakerDAO operates differently from typical lending platforms by offering a unique system centered around generating DAI stablecoin. Users lock collateral (primarily Ethereum) into Maker’s system to mint DAI, which maintains its peg to the US dollar through algorithmic mechanisms and collateral auctions. Rather than traditional borrowing against collateral, this process creates a decentralized stablecoin that users can use elsewhere, then repay to release their locked collateral.

Cream Finance focuses on serving users excluded by other protocols, particularly in emerging markets. The platform offers lending and borrowing for a wide range of assets, including some that other major platforms don’t support. However, Cream has experienced several security incidents, resulting in significant losses, which potential users should consider when evaluating the platform.

Kava operates as a Cosmos ecosystem lending platform offering cross-chain lending services. Unlike Ethereum-based protocols, Kava uses its own blockchain with a unique consensus mechanism that aims to provide faster transactions and lower fees. The platform supports various assets across different blockchains, making it attractive for users with diverse cryptocurrency portfolios.

Risks Involved with DeFi Lending

DeFi lending offers attractive returns, but understanding the risks is essential before participating. Several factors can result in losses, sometimes severe.

Smart Contract Risk represents the possibility that code bugs or vulnerabilities could be exploited by attackers. While major DeFi protocols have undergone extensive security audits, exploits still occur. In 2021 alone, DeFi hacks resulted in billions of dollars in losses, with attackers targeting both lending platforms and the broader ecosystem. Even audited contracts have suffered vulnerabilities that went undetected.

Liquidation Risk affects borrowers when their collateral value drops relative to their loan. During periods of high market volatility, cryptocurrency prices can drop dramatically within minutes, triggering automatic liquidations before borrowers have opportunity to add collateral. Many users have lost significant portions of their holdings this way, particularly during the sharp market corrections of 2022.

Impermanent Loss affects liquidity providers in decentralized exchanges rather than direct lending, but similar principles apply to DeFi participation. When you supply assets to protocols that use those assets elsewhere, price changes between your deposited assets and what you receive upon withdrawal can result in losses compared to simply holding the assets.

Platform Risk encompasses the possibility that a lending protocol could fail due to governance attacks, economic vulnerabilities, or abandoned development. While established platforms like Aave and Compound have strong track records, the DeFi space remains competitive and new platforms launch regularly with varying levels of robustness.

Regulatory Uncertainty continues to shadow DeFi lending globally. Different jurisdictions approach decentralized finance differently, and future regulations could impact how these platforms operate or restrict access for users in certain countries. Germany, your target market, has been relatively crypto-friendly, but regulatory changes remain possible.

How to Get Started with DeFi Lending

Beginning your DeFi lending journey requires careful preparation and a methodical approach to managing risk.

Step 1: Set Up a Compatible Wallet — You’ll need a Web3 wallet like MetaMask, Rabby, or Ledger Live to interact with DeFi protocols. These wallets store your private keys and allow you to connect to decentralized applications. Hardware wallets like Ledger devices provide additional security for larger holdings.

Step 2: Acquire Cryptocurrency — You’ll need funds to deposit. Most users start with Ethereum or stablecoins since these assets have the deepest liquidity pools and most established markets. Purchase cryptocurrency from reputable exchanges that support your jurisdiction—major exchanges like Coinbase, Kraken, or Binance typically serve German users well.

Step 3: Transfer to Your Wallet — Send your purchased cryptocurrency from the exchange to your Web3 wallet. Always double-check the receiving address, as cryptocurrency transactions cannot be reversed. Start with small amounts while learning.

Step 4: Connect to a Lending Platform — Visit the official website of your chosen platform and click “Connect Wallet.” Your Web3 wallet will prompt you to approve the connection. Ensure you’re on the legitimate platform—bookmark official sites and verify URLs carefully to avoid phishing attacks.

Step 5: Supply Assets — Navigate to the supply section of the platform and select the asset you want to deposit. Approve the token for use with the protocol, then confirm your deposit transaction. You’ll begin earning interest immediately after the transaction confirms.

Step 6: Manage Your Position — Regularly monitor your deposits, interest earned, and collateral health if you’ve borrowed against your deposits. Set up alerts for significant price movements in your collateral assets to avoid unexpected liquidations.

Comparing Platform Features

When choosing a DeFi lending platform, several factors warrant consideration based on your specific needs and risk tolerance.

| Platform | Supported Assets | Unique Features | Security Audits |

|---|---|---|---|

| Aave | 20+ assets | Flash loans, credit delegation | Multiple audits, bug bounty |

| Compound | 10+ assets | COMP token rewards, governance | Audited, proven track record |

| MakerDAO | ETH, Stablecoins | DAI stablecoin generation | Extensive audits, conservative approach |

| Cream Finance | 30+ assets | Emerging market focus | Multiple incidents, lower security history |

| Kava | Cross-chain | Multi-chain support, lower fees | Audited, Cosmos ecosystem |

For Beginners: Aave and Compound offer the best combination of security, ease of use, and educational resources. Their interfaces are relatively intuitive, and their track records inspire confidence.

For Maximum Returns: Smaller or newer platforms sometimes offer higher APYs to attract liquidity, but these increased returns come with elevated risks. Approach such opportunities with caution and only commit amounts you’re willing to lose entirely.

For Stablecoin Lending: If your goal is earning yield on stablecoins like USDC or DAI, most platforms offer these options with APYs typically ranging from 3% to 8%, significantly higher than traditional savings accounts.

Frequently Asked Questions

Is DeFi lending safe?

DeFi lending carries several risks including smart contract vulnerabilities, liquidation during price volatility, and platform failure. Major platforms like Aave and Compound have strong security histories but no DeFi platform can guarantee safety. Only use money you can afford to lose, start with small amounts, and thoroughly understand the risks before depositing significant funds.

Do I need to pay taxes on DeFi lending earnings in Germany?

Yes, income from DeFi lending is generally taxable in Germany. Interest earned from cryptocurrency lending is treated as income and subject to income tax. Additionally, capital gains may apply when withdrawing or selling earned tokens. German tax laws regarding cryptocurrency remain evolving, so consulting a tax professional familiar with crypto taxation is advisable.

What happens if the cryptocurrency I borrowed drops to zero?

If the asset you borrowed becomes worthless, you don’t need to repay it—you simply keep what you borrowed. However, this scenario is extremely rare for major cryptocurrencies. More importantly, if your collateral drops significantly, you face liquidation before the borrowed asset reaches zero. Borrowed assets typically retain some value, and you must eventually repay the loan plus interest.

Can I lose more than I deposit as collateral?

In theory, over-collateralization should prevent this, but during extreme market conditions with rapid price drops and network congestion, liquidations may execute at unfavorable prices, potentially resulting in losing more than initially deposited. Additionally, accrued interest increases your debt over time, requiring more collateral to maintain your position.

How do I choose which cryptocurrency to lend?

Consider factors including the asset’s volatility, your belief in its long-term value, and the platform’s supported assets. Stablecoins offer lower liquidation risk but typically provide lower yields. Volatile assets like Ethereum offer higher yields but require more careful collateral management. Diversifying across multiple assets and platforms reduces single-point failures.

What’s the minimum amount needed to start DeFi lending?

There isn’t an official minimum, but transaction fees (gas costs on Ethereum can exceed $10-50 during busy periods) make small deposits impractical. Depositing at least several hundred euros worth of cryptocurrency generally makes economic sense after accounting for gas costs. Layer 2 networks like Polygon or Arbitrum offer lower fees, enabling smaller deposits.

Conclusion

DeFi lending platforms represent a significant innovation in financial services, offering ways to earn interest on cryptocurrency holdings and access liquidity without traditional banking intermediaries. The ability to earn yields significantly higher than conventional savings accounts, combined with around-the-clock accessibility and algorithmic transparency, appeals to many cryptocurrency users.

However, this new paradigm comes with substantial risks that traditional finance doesn’t present. Smart contract vulnerabilities, liquidation exposure, and regulatory uncertainty require careful consideration. Beginning with established platforms like Aave or Compound, starting with small amounts, and thoroughly understanding how these systems work before committing significant funds represents the prudent approach.

As you gain experience, exploring different strategies—providing liquidity across multiple platforms, experimenting with borrowing against collateral to leverage positions, or diversifying across various assets—can potentially increase your returns. But always remember that the DeFi space evolves rapidly, and yesterday’s safe platform may face challenges tomorrow.

The fundamental promise of DeFi—financial services accessible to anyone with an internet connection—remains compelling. By understanding both the opportunities and risks, you can make informed decisions about whether DeFi lending fits into your financial strategy.