Blockchain technology has become one of the most discussed innovations of the past decade, yet many people still find it confusing or intimidating. At its core, blockchain is a way to record information that is transparent, secure, and impossible to alter retroactively. Unlike traditional databases controlled by a single entity, blockchain distributes its data across countless computers worldwide, creating a decentralized system where trust is built into the technology itself rather than relying on banks, governments, or other intermediaries.

This fundamental shift in how we think about data and trust has implications far beyond cryptocurrency, affecting industries from healthcare and supply chain management to voting systems and intellectual property. Understanding how blockchain works doesn’t require a computer science degree—it simply requires breaking down the concept into its core components and seeing how they fit together.

What Actually Is a Blockchain?

A blockchain is a distributed digital ledger that records transactions across many computers in a way that makes the records extremely difficult to alter retroactively. The term “blockchain” comes from how the technology structures data: individual batches of transactions called “blocks” are linked together in a chronological chain, creating an immutable history of every transaction ever made on the network.

Think of a blockchain like a shared Google Document that everyone with access can view but no one can secretly change. When someone adds new information, everyone else with a copy of the document sees the change instantly. If someone tries to go back and alter an earlier entry, the network rejects it because the majority of participants can verify that the original entry was different. This transparency and immutability are what make blockchain fundamentally different from traditional databases.

The technology emerged in 2008 when an individual or group using the pseudonym Satoshi Nakamoto published the Bitcoin whitepaper, introducing blockchain as the underlying infrastructure for a peer-to-peer digital currency. However, the concept of cryptographically secured, distributed ledgers had been explored by researchers since the 1990s. Bitcoin simply became the first practical implementation that solved the longstanding “double-spend problem”—the challenge of preventing someone from spending the same digital currency twice—without requiring a trusted third party like a bank.

The Building Blocks: How Blocks Work

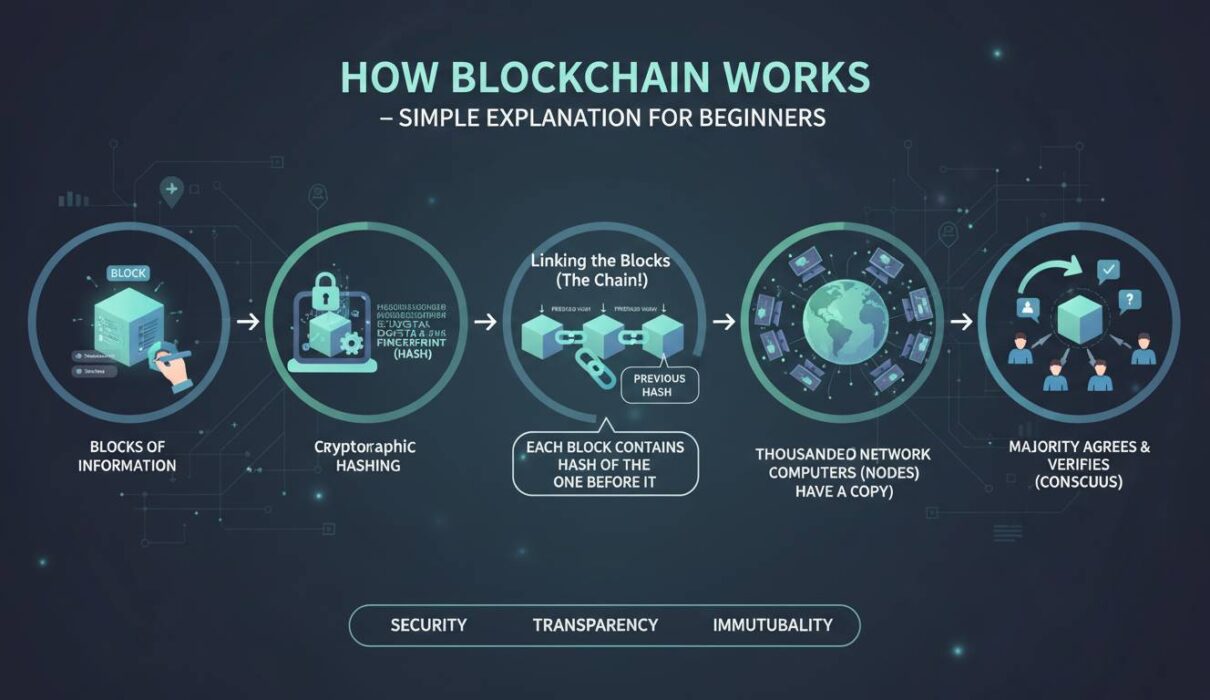

To understand how blockchain functions, you need to understand what goes inside each “block” and how these blocks connect to one another. Every block contains three essential elements: data, a hash, and the hash of the previous block.

The data stored inside a block varies depending on the blockchain’s purpose. In Bitcoin’s case, a block contains information about sender and receiver wallet addresses, the amount transferred, and a timestamp. In more complex blockchain applications, the data might include legal contracts, medical records, or supply chain information.

A hash is like a digital fingerprint—a unique string of characters generated by a mathematical function that converts any input into a fixed-size output. If you change even a single character in the block’s data, the hash changes completely. This is crucial because each block includes its own hash and the hash of the previous block, creating a cryptographic chain. If someone tries to tamper with historical data, they would need to recalculate the hash for that block and every subsequent block—computationally impractical given the sheer number of computers maintaining the network.

This mathematical linking mechanism is what gives blockchain its security. Changing historical records isn’t just difficult or expensive; it’s effectively impossible without detection. The network constantly verifies that all copies of the blockchain match, rejecting any version that doesn’t conform to the established chain.

The Chain Reaction: Why It’s Unbreakable

The real power of blockchain emerges from its decentralized structure. Rather than storing one copy of the database on a central server, blockchain networks maintain thousands of identical copies across computers (called “nodes”) spread around the world. When a new block is added, every node receives and verifies the update independently.

This distribution creates several powerful security properties. First, there is no single point of failure—if one computer (or even thousands) goes offline or gets hacked, the network continues operating because other copies exist everywhere. Second, tampering becomes exponentially difficult because an attacker would need to control the majority of the network’s computing power to alter the consensus record—a requirement known as “51% attack” resistance. For major blockchains like Bitcoin, this would require astronomical resources, making such attacks practically unthinkable.

The consensus mechanism that keeps all these distributed computers in sync varies between blockchains. Bitcoin uses “Proof of Work,” where computers (miners) compete to solve complex mathematical puzzles, and the winner gets to add the next block. This process consumes significant energy but has proven remarkably secure over more than a decade of operation. Other blockchains use “Proof of Stake,” where validators put up cryptocurrency as collateral and are chosen to create new blocks based on how much they have staked, consuming far less energy than Proof of Work systems.

According to data from the University of Cambridge, Bitcoin’s network currently consumes approximately 150 terawatt-hours of electricity annually—comparable to some small countries—though this energy consumption is what secures trillions of dollars in value and processes millions of transactions. Ethereum, the second-largest blockchain, transitioned to Proof of Stake in 2022, reducing its energy consumption by approximately 99.95%.

Real-World Applications Beyond Cryptocurrency

While cryptocurrency remains blockchain’s most famous application, the technology’s ability to create trustless, transparent records has sparked innovation across virtually every industry.

Supply Chain Management represents one of blockchain’s most practical use cases. Companies like Walmart have implemented blockchain systems to track food products from farm to shelf, reducing the time it takes to trace the origin of contaminated products from days to seconds. This transparency helps identify problems quickly, improve food safety, and build consumer confidence.

Healthcare is another sector transformed by blockchain. Medical records stored on blockchain can be securely shared between hospitals, insurers, and patients without risking data breaches or unauthorized modifications. Patients gain control over who can access their sensitive information, while healthcare providers benefit from having a complete, unchangeable medical history. Estonia’s national health system has been a pioneer in this area, using blockchain technology to secure health records since 2012.

Voting systems benefit from blockchain’s immutability and transparency. Several countries, including Estonia and Switzerland, have experimented with blockchain-based voting that allows citizens to verify their votes were counted while preventing tampering with election results. Each vote becomes a permanent, verifiable transaction on an immutable ledger.

Real estate transactions, traditionally requiring multiple intermediaries, lawyers, and weeks of processing, can potentially be streamlined through blockchain. Smart contracts—self-executing programs stored on the blockchain that automatically enforce agreement terms—can automate property transfers, ensuring funds aren’t released until all conditions are met. This reduces fraud, speeds up transactions, and cuts legal costs.

Intellectual property and NFTs represent another growing application. Artists and creators can use blockchain to prove ownership of digital works, establish provenance, and receive royalties automatically whenever their work is resold. This addresses long-standing challenges in the digital art world where reproduction is trivial and ownership is difficult to verify.

Public vs Private Blockchains: What’s the Difference?

Not all blockchains operate the same way. The two primary categories—public and private—serve different purposes and offer distinct advantages.

Public blockchains like Bitcoin and Ethereum are open networks where anyone can participate. You can read the ledger, submit transactions, or (in many cases) help validate transactions by running node software. These networks prioritize decentralization and censorship resistance, making them ideal for applications where no single entity should control the system. The trade-off is often slower transaction speeds and greater energy consumption, as reaching consensus among thousands of unknown participants requires more computation and communication.

Private blockchains restrict participation to invited members only. A company might create a private blockchain to track internal supply chain data or manage employee records. These networks offer faster transactions and greater control but sacrifice the decentralization that makes public blockchains resistant to censorship and tampering. Critics argue that private blockchains essentially replicate the limitations of traditional databases while adding unnecessary complexity.

Consortium blockchains represent a middle ground, where a group of organizations jointly operate the network. Financial institutions, for example, might collectively maintain a blockchain for interbank settlements, sharing control while maintaining some centralization. This approach balances the benefits of blockchain with the need for regulatory compliance and operational efficiency.

The choice between these types depends entirely on the specific use case. A decentralized cryptocurrency requires a public blockchain; a private company’s internal records might work better with a private chain. Understanding this distinction helps avoid the common mistake of assuming one blockchain type suits all purposes.

Getting Started: Your First Blockchain Interaction

If you’re new to blockchain, you don’t need to run a node or understand complex cryptography to interact with the technology. Many accessible entry points exist for ordinary users.

Cryptocurrency wallets represent the most common way people engage with blockchain technology. A wallet doesn’t actually store cryptocurrency—it stores the cryptographic keys that prove you control a particular balance on the blockchain. Wallets come in various forms: mobile apps, browser extensions, hardware devices (which store keys offline for maximum security), or even paper documents containing your keys.

To get started, you would download a reputable wallet app, generate a new set of keys (usually represented as a “seed phrase” of 12 or 24 words), and back up that seed phrase securely. With your wallet set up, you can receive cryptocurrency from anyone, send it to others, and interact with blockchain-based applications.

Exploring blockchain explorers offers a way to view blockchain data without needing any software. Websites like Etherscan for Ethereum or Blockchain.com’s block explorer for Bitcoin allow you to search for specific transactions, view current block numbers, see how much energy the network is consuming, and track any public address’s transaction history. Walking through your own transactions on a block explorer provides an intuitive understanding of how the system works.

Educational platforms have emerged to help beginners understand blockchain concepts without financial risk. Games like “CryptoZombies” teach smart contract programming through interactive lessons, while platforms like Binance Academy offer free courses covering everything from basic blockchain concepts to advanced cryptography.

Common Misconceptions About Blockchain

Several persistent myths about blockchain deserve clarification, as they often lead to confusion or poor decision-making.

Myth: Blockchain is the same as Bitcoin. Bitcoin is simply one application of blockchain technology—the first and most famous one. Blockchain is the underlying infrastructure; Bitcoin is a specific implementation of a cryptocurrency built on that infrastructure. Many other cryptocurrencies and non-currency applications exist independently of Bitcoin.

Myth: Blockchain is always secure. While blockchain itself is cryptographically secure, the applications built on top of it are not immune to vulnerabilities. Cryptocurrency exchanges have been hacked, smart contracts have contained bugs that led to massive financial losses, and users have lost funds through phishing attacks and scams. Security depends on implementation, not just the underlying technology.

Myth: Blockchain is completely anonymous. Most blockchains are actually pseudonymous rather than anonymous. Transactions are publicly visible and linked to addresses, which can potentially be traced to real-world identities through exchange records, IP addresses, or spending patterns. Privacy-focused cryptocurrencies exist, but they represent a small portion of the overall ecosystem.

Myth: Blockchain is inherently efficient. While blockchain excels at creating trustless, immutable records, this comes with trade-offs. The decentralized verification process is inherently slower than centralized alternatives, and systems like Bitcoin’s Proof of Work consume substantial energy. Blockchain solves specific problems; it’s not a universal solution that outperforms traditional databases in all scenarios.

The Future of Blockchain Technology

The blockchain ecosystem continues evolving rapidly, with several trends shaping its future direction.

Layer 2 solutions aim to address blockchain’s scalability limitations by processing transactions on secondary platforms while periodically settling them on the main blockchain. These solutions—like Bitcoin’s Lightning Network or Ethereum’s various scaling protocols—enable far more transactions per second while maintaining security. The Lightning Network alone has grown to hold over 5,000 BTC in capacity, enabling millions of small transactions that would be impractical on the main Bitcoin network.

Interoperability between different blockchains is improving, allowing assets and information to flow across networks that previously operated in isolation. Cross-chain bridges and protocols like Polkadot and Cosmos aim to create an “internet of blockchains” where different networks can communicate and transfer value seamlessly.

Regulation continues developing worldwide. The European Union’s MiCA (Markets in Crypto-Assets) regulation, fully implemented in 2024, creates a comprehensive framework for cryptocurrency providers operating within the EU. Germany’s approach has been relatively supportive, permitting banks to custody cryptocurrency since 2020 and providing clarity on taxation that treats cryptocurrency similarly to other private sales.

Enterprise adoption is accelerating as major corporations recognize practical applications. From JPMorgan’s Onyx platform for interbank payments to IBM’s food tracking systems, blockchain is moving beyond speculation toward real-world utility. This enterprise adoption often occurs on private or consortium blockchains tailored to specific business needs.

Frequently Asked Questions

What is blockchain in the simplest terms?

Blockchain is a digital record-keeping system where information is stored in “blocks” that are linked together in a “chain.” Once information is added, it’s extremely difficult to change retroactively. The record is shared across many computers, so no single person or company controls it.

Do I need to understand coding to use blockchain?

No, most blockchain interactions don’t require coding knowledge. You can use cryptocurrency wallets, participate in decentralized applications, and transfer digital assets through user-friendly interfaces similar to traditional banking apps.

Is blockchain the same as cryptocurrency?

No, cryptocurrency is just one application of blockchain technology. Blockchain is the underlying infrastructure, while cryptocurrencies like Bitcoin and Ethereum are digital currencies built on top of that infrastructure.

How secure is blockchain technology?

Blockchain is considered highly secure due to its cryptographic structure and decentralization. However, individual applications built on blockchain (like exchanges or smart contracts) can have vulnerabilities. User security practices, such as protecting your private keys, remain essential.

Can blockchain transactions be reversed?

Generally, no—one of blockchain’s core features is immutability. Once a transaction is confirmed and added to the blockchain, it cannot be reversed. This is by design and what makes blockchain useful for creating permanent, trustworthy records.

What’s the difference between Bitcoin and Ethereum?

Bitcoin was created primarily as a digital currency and store of value, using a relatively simple blockchain focused on transactions. Ethereum is a programmable platform that allows developers to build applications and smart contracts on its blockchain, enabling far more complex use cases beyond simple value transfer.

Conclusion

Blockchain technology represents a fundamental shift in how we establish trust and record information. By distributing data across networks, using cryptographic verification, and creating immutable records, blockchain enables new forms of collaboration and transparency that were previously impossible. While the technology started with cryptocurrency, its applications have expanded far beyond digital money into healthcare, supply chains, voting systems, and countless other domains.

For beginners, the key is understanding that blockchain isn’t magic—it’s a carefully designed system that uses established cryptographic principles to solve specific problems around trust, transparency, and coordination. Whether you want to use cryptocurrency, build applications, or simply understand why blockchain matters, the concepts covered here provide a solid foundation for further exploration.

As the technology matures, expect to see more practical applications emerge, better integration with existing systems, and clearer regulatory frameworks. The blockchain revolution is still unfolding, and understanding its fundamentals positions you to navigate this changing landscape with confidence.