Blockchain technology has become one of the most discussed innovations of the twenty-first century, yet many people still find it confusing or intimidating. At its core, blockchain is a revolutionary way to store and share information that eliminates the need for traditional intermediaries like banks or governments to verify transactions. This distributed ledger technology enables trustless peer-to-peer exchanges, fundamentally changing how we think about digital ownership, financial systems, and data security.

Unlike conventional databases controlled by a single entity, blockchain operates across thousands of computers simultaneously, making it nearly impossible to alter past records without detection. Whether you’re interested in cryptocurrencies, supply chain management, digital identity verification, or smart contracts, understanding blockchain provides valuable insight into the digital transformation reshaping industries worldwide.

The Fundamentals: How Blockchain Actually Works

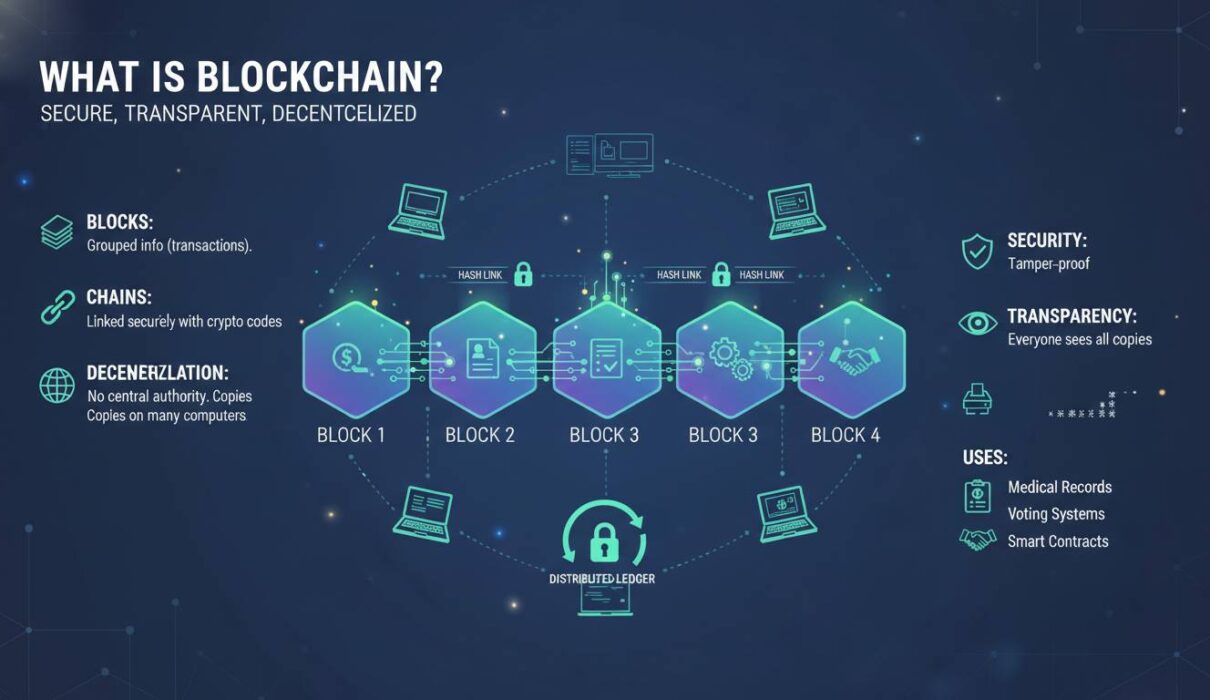

To understand blockchain, imagine a digital notebook that everyone in a network can read and write to, but nobody can erase or修改 (modify) what has already been written. This notebook consists of blocks of data chained together chronologically, hence the name “blockchain.” Each block contains three critical elements: data, a hash (a unique digital fingerprint), and the hash of the previous block.

When a new transaction occurs—such as sending cryptocurrency or recording a document—the information is bundled into a block and broadcast to the network. Computers called nodes verify the transaction using complex mathematical algorithms. Once the majority of nodes agree that the transaction is valid, the block is added to the existing chain. This consensus mechanism ensures that all participants have an identical copy of the ledger, eliminating the need for a central authority to mediate trust.

The genius of blockchain lies in its immutability. Because each block contains the hash of its predecessor, changing any historical record would require recalculating every subsequent block—a computationally impossible task given the vast network of validators. This makes blockchain exceptionally secure against fraud and tampering, a feature that has attracted interest from financial institutions, healthcare providers, and governments worldwide.

Why Blockchain Matters: Key Advantages Explained

The revolutionary potential of blockchain stems from several distinctive characteristics that set it apart from traditional database systems. Understanding these advantages helps explain why industries worldwide are investing billions in blockchain implementation.

Decentralization represents blockchain’s most transformative feature. Rather than storing data on a single server controlled by one organization, blockchain distributes identical copies across thousands of nodes globally. This architectural choice means there is no single point of failure— Even if many computers go offline, the network continues functioning as long as one node remains active. According to a 2023 report by Deloitte, 76% of surveyed executives identified decentralization as blockchain’s primary value proposition for their industries.

Transparency comes naturally to public blockchains, where anyone can view transaction history. While this might seem counterintuitive for privacy-conscious applications, transparency actually increases accountability. Every transaction creates a permanent, publicly verifiable record that cannot be retroactively altered, reducing corruption and increasing trust between parties who have never met.

Security emerges from cryptography and consensus mechanisms. Blockchain uses advanced cryptographic techniques to protect data, while the distributed validation process makes unauthorized changes extraordinarily difficult. A 2022 IBM study found that blockchain-based supply chain solutions reduced fraud incidents by 40% compared to traditional tracking methods.

Efficiency improves dramatically by removing intermediaries. Cross-border payments that traditionally take 3-5 business days can settle in minutes on blockchain networks. The World Bank estimates that blockchain could reduce remittance costs globally by approximately $16 billion annually by removing middlemen fees.

Blockchain vs Traditional Databases: Understanding the Differences

Many people struggle to grasp blockchain because they compare it incorrectly to familiar technologies like standard databases. The fundamental distinction lies in how data is organized, verified, and controlled.

Traditional databases use a client-server architecture where a central administrator has complete control over reading, writing, and deleting information. If the database administrator (or a hacker who compromises their credentials) chooses to modify records, they can do so without limitation. This centralized control model has served businesses well for decades but creates single points of failure and requires expensive trust-building mechanisms.

Blockchain inverts this paradigm entirely. No single party controls the network; instead, consensus among distributed participants determines what gets added to the ledger. Once information enters the blockchain, it becomes permanent and tamper-proof. The following comparison illustrates these differences:

| Characteristic | Traditional Database | Blockchain |

|---|---|---|

| Control | Centralized authority | Distributed network |

| Data Modification | Can be altered freely | Nearly impossible to change |

| Transaction Speed | Faster for single operations | Slower due to consensus |

| Transparency | Limited access | Public or permissioned viewing |

| Energy Consumption | Lower generally | Varies by consensus mechanism |

| Best Use Cases | Internal data, rapid updates | Cross-party trust, value transfer |

For internal business operations requiring rapid updates and administrative control, traditional databases remain appropriate. Blockchain shines when multiple parties who don’t fully trust each other need to share verified information without requiring an intermediary.

Types of Blockchains: Public, Private, and Consortium

Not all blockchains operate identically. The technology has evolved to address different use cases, resulting in several distinct categories that serve various organizational needs.

Public blockchains like Bitcoin and Ethereum are open networks where anyone can participate as a node, validate transactions, or read the ledger. These networks prioritize maximum decentralization and censorship resistance, making them ideal for cryptocurrencies and decentralized applications. However, public blockchains typically sacrifice transaction speed and privacy for their open nature. Bitcoin processes approximately 7 transactions per second, while Ethereum handles around 15-30 transactions per second before recent upgrades.

Private blockchains restrict participation to approved organizations or individuals. These permissioned networks offer faster transaction processing and greater privacy controls, making them attractive to enterprises managing sensitive data. Hyperledger Fabric and R3 Corda represent popular private blockchain platforms. Critics argue private blockchains sacrifice the trustless benefits that make public blockchains valuable, essentially recreating traditional centralized systems with added technological complexity.

Consortium blockchains represent a middle ground, operated by a group of organizations rather than a single entity or the general public. These networks combine decentralization benefits with the efficiency and privacy enterprises require. Consortium blockchains have gained significant traction in finance, supply chain, and healthcare applications where multiple companies need to share data securely without a single controlling party.

The choice between blockchain types depends entirely on use case requirements. A cryptocurrency needs public transparency, while a hospital system sharing patient records across organizations might benefit from consortium or private blockchain architecture.

Real-World Applications Beyond Cryptocurrency

While cryptocurrency remains blockchain’s most visible application, the technology’s utility extends far beyond digital money. Industries worldwide are discovering innovative ways to leverage blockchain’s unique properties for problems that traditional technology struggles to solve.

Supply Chain Management represents one of blockchain’s most promising applications. Walmart has pioneered blockchain for food traceability, reducing the time needed to track produce from farm to shelf from 7 days to 2.2 seconds. This visibility helps identify contamination sources quickly, reduces food waste, and ensures ethical sourcing claims are verifiable. A 2023 study by the Food Standards Agency found that blockchain-enabled supply chains reduced fraudulent organic certification claims by 65%.

Healthcare benefits enormously from blockchain’s ability to create secure, interoperable patient records. Medical data currently exists in fragmented silos across hospitals, clinics, and insurance companies. Blockchain could enable patients to control who accesses their health information while ensuring data integrity. IBM and MedRec have developed blockchain-based electronic health record systems that give patients granular consent controls over their medical history.

Digital Identity Verification addresses a growing problem in our increasingly online world. Traditional identity systems require sharing sensitive personal information with numerous service providers, creating privacy risks and inefficiencies. Blockchain enables self-sovereign identity, where users maintain portable credentials verified by trusted issuers without exposing underlying data. Estonia’s government has implemented blockchain technology to secure citizen health records and provide tamper-proof audit trails for government data.

Real Estate transactions typically involve numerous intermediaries—lawyers, title companies, banks, and notaries—each adding time and cost. Blockchain can streamline property transfers by creating a single source of truth for ownership records, reducing transaction times from weeks to days while eliminating redundant verification steps. Propy, a blockchain real estate platform, has facilitated over $3 billion in property transactions globally.

Smart Contracts: Blockchain’s Programmable Revolution

Smart contracts represent blockchain’s most transformative capability beyond simple value transfer. These self-executing programs automatically enforce agreement terms when predetermined conditions are met, eliminating the need for intermediaries and reducing the potential for disputes.

Imagine renting an apartment through a traditional system: you pay a security deposit, sign paper agreements, hand over keys, and hope the landlord returns your deposit after you move out. Now imagine this process on a blockchain: you send cryptocurrency to a smart contract that holds the funds, the contract automatically releases your apartment access credentials, and upon move-out, the contract verifies no damage occurred (potentially through IoT sensor data) before releasing your deposit instantly.

This programmable capability opens possibilities across countless industries. Insurance policies could automatically pay claims when verified events occur. Supply chain payments could trigger upon GPS confirmation of delivery. Royalty distributions could flow automatically to creators whenever their work generates revenue. According to a 2024 report by Chainlink, the smart contract market is projected to reach $300 billion by 2030 as enterprises recognize automation benefits.

Ethereum, launched in 2015, pioneered smart contract functionality and remains the dominant platform for decentralized applications. Its virtual machine executes code exactly as written, removing human interpretation from contract enforcement. While this reliability creates powerful possibilities, it also means bugs in smart contract code can have permanent, irreversible consequences—a lesson learned painfully through various high-profile blockchain hacks that have resulted in billions of dollars in losses.

Common Misconceptions About Blockchain Technology

Despite growing awareness, blockchain remains widely misunderstood. Addressing these misconceptions helps separate realistic expectations from hype that has characterized much public discourse.

Misconception 1: Blockchain is inherently private and anonymous. While some cryptocurrencies like Monero or Zcash emphasize privacy, most public blockchains create permanently visible transaction records linked to wallet addresses. Analysis firms regularly trace transactions to identify entities, making blockchain更适合 (more suitable) for transparency than secrecy. Organizations requiring privacy must implement additional encryption layers or choose permissioned blockchain designs.

Misconception 2: Blockchain is automatically more efficient than existing systems. Blockchain introduces coordination overhead that traditional databases avoid. For single-organization internal processes, conventional databases remain faster and more cost-effective. Blockchain’s efficiency gains appear primarily in multi-party scenarios where trust between participants is limited and intermediaries currently extract significant rents.

Misconception 3: All blockchains consume enormous energy. Energy consumption varies dramatically by consensus mechanism. Bitcoin’s proof-of-work protocol does require substantial electricity, leading to valid environmental criticism. However, Ethereum completed “The Merge” in 2022, reducing energy consumption by approximately 99.95% through switching to proof-of-stake. Many enterprise blockchains never used proof-of-work at all, operating efficiently on alternative consensus mechanisms.

Misconception 4: Blockchain is only for cryptocurrency. While cryptocurrency remains important, major corporations, governments, and NGOs increasingly deploy blockchain for non-financial applications including supply chain tracking, digital identity, voting systems, and intellectual property management. The global blockchain market is expected to reach $1.7 trillion by 2030, with non-cryptocurrency applications representing a growing majority.

Getting Started: Practical Ways to Engage With Blockchain

For readers curious about experiencing blockchain firsthand, several accessible entry points exist ranging from passive observation to active participation.

Using cryptocurrency wallets provides the most direct blockchain interaction. Wallets like MetaMask, Trust Wallet, or Coinbase Wallet let users send and receive digital assets, interact with decentralized applications, and experience blockchain’s transparency through block explorers like Etherscan, which allows viewing any transaction on public blockchains.

Exploring decentralized applications demonstrates blockchain’s practical capabilities beyond financial speculation. Platforms like Uniswap (decentralized exchange), OpenSea (digital collectibles), and Aave (decentralized lending) showcase different blockchain use cases. These applications operate without traditional companies, governed instead by community token holders.

Learning basic technical concepts helps demystify blockchain further. Understanding keys (public and private), hashes, consensus mechanisms, and wallet addresses provides foundation for deeper exploration. Free resources from platforms like Coinbase Learn, Binance Academy, and various university online courses offer accessible educational content.

Following industry developments keeps pace with rapid evolution. Podcasts like “The Defiant” and “Bankless,” newsletters like “The Block” and “CoinDesk,” and conferences like ETHDenver and Paris Blockchain Week provide ongoing education for interested participants.

Frequently Asked Questions

What is blockchain in the simplest terms?

Blockchain is a shared digital notebook that thousands of computers maintain together. Once information gets written into it, nobody can erase or change it. Think of it like a highly secure, transparent record-keeping system where everyone can see what happened but no single person controls the records.

How is blockchain different from Bitcoin?

Bitcoin is a digital currency, while blockchain is the underlying technology that makes Bitcoin work. Blockchain is the infrastructure; Bitcoin is just one application of that infrastructure. Many other cryptocurrencies and non-currency applications use blockchain technology.

Is blockchain secure?

Yes, blockchain is considered highly secure due to its decentralized nature and cryptographic protection. To alter any past record, an attacker would need to control and modify the majority of network computers simultaneously, which becomes computationally infeasible as networks grow larger. However, individual applications built on blockchain can have security vulnerabilities through poor coding or user error.

Do I need technical skills to use blockchain?

No, many blockchain applications now offer user-friendly interfaces that abstract technical complexity. Popular cryptocurrency exchanges allow buying, selling, and holding digital assets with interfaces similar to traditional banking apps. However, understanding basic concepts like private keys and wallet security remains important to avoid losing funds.

Will blockchain replace traditional banks?

Blockchain is more likely to complement and transform existing financial services rather than completely replace banks. Many financial institutions now embrace blockchain for faster settlement, reduced costs, and new services. Traditional banks provide services—fraud protection, customer support, regulatory compliance—that blockchain alone cannot fully replicate.

How long does a blockchain transaction take?

Transaction times vary significantly by blockchain network and current activity. Bitcoin transactions typically confirm within 10-60 minutes, while Ethereum transactions usually complete in seconds to minutes during normal network conditions. Some blockchain networks offer near-instant finality, though this often involves trade-offs with decentralization.